***This content has been updated. You can read the most recent version of this article here.***

In a nutshell:

- Kiwi are missing out on roughly $2 billion of interest each year on “lazy” money sitting in their transaction accounts.

- We’ve stacked up Aotearoa’s best and worst savings accounts to help you unlock your share.

- Consider Squirrel’s On-Call account as an alternative.

Today there’s $44 billion dollars of Kiwi money sitting in transaction accounts, where almost all of it is earning 0% p.a.

That was fine 18 months ago, when interest rates were close to zero.

Back then, with the Official Cash Rate (OCR) at 0.25%, you weren’t losing out on too much if you left a big chunk of your money sitting idly in a transaction account.

But oh boy, things have changed.

Today the OCR is 5.25%. So, on that $44 billion we’ve got sitting in transaction accounts, the potential interest earnings have skyrocketed.

And if it’s not going to Kiwi, who’s reaping the reward?

You guessed it – the banks.

On any of that $44 billion that the banks are holding in reserve, they’ll be earning 5.25% per annum (in line with the OCR) – paid to them by the Reserve Bank.

If they’ve lent it out to other Kiwi in the form of home loans, business loans, credit cards, or other debt, they could be earning a whole lot more.

Crunching the numbers, that means the banks are earning *at least* $2.2 billion a year on funds held in OUR transaction accounts.

That’s over $6 million per day.

Money which, if it was back in Kiwi pockets, wouldn’t go amiss in this cost-of-living crisis.

So, if you’ve got more than about $1,000 in your transaction account today (or thereabouts, depending on how much you need to cover everyday transactions), then you should move it to a savings account. ASAP!

There’s up to a couple of billion dollars waiting for New Zealanders, collectively.

What’s the best option right now?

In short, it depends on how quickly you need might need access to your money. The longer you can commit to locking it away for, the more interest you’ll earn.

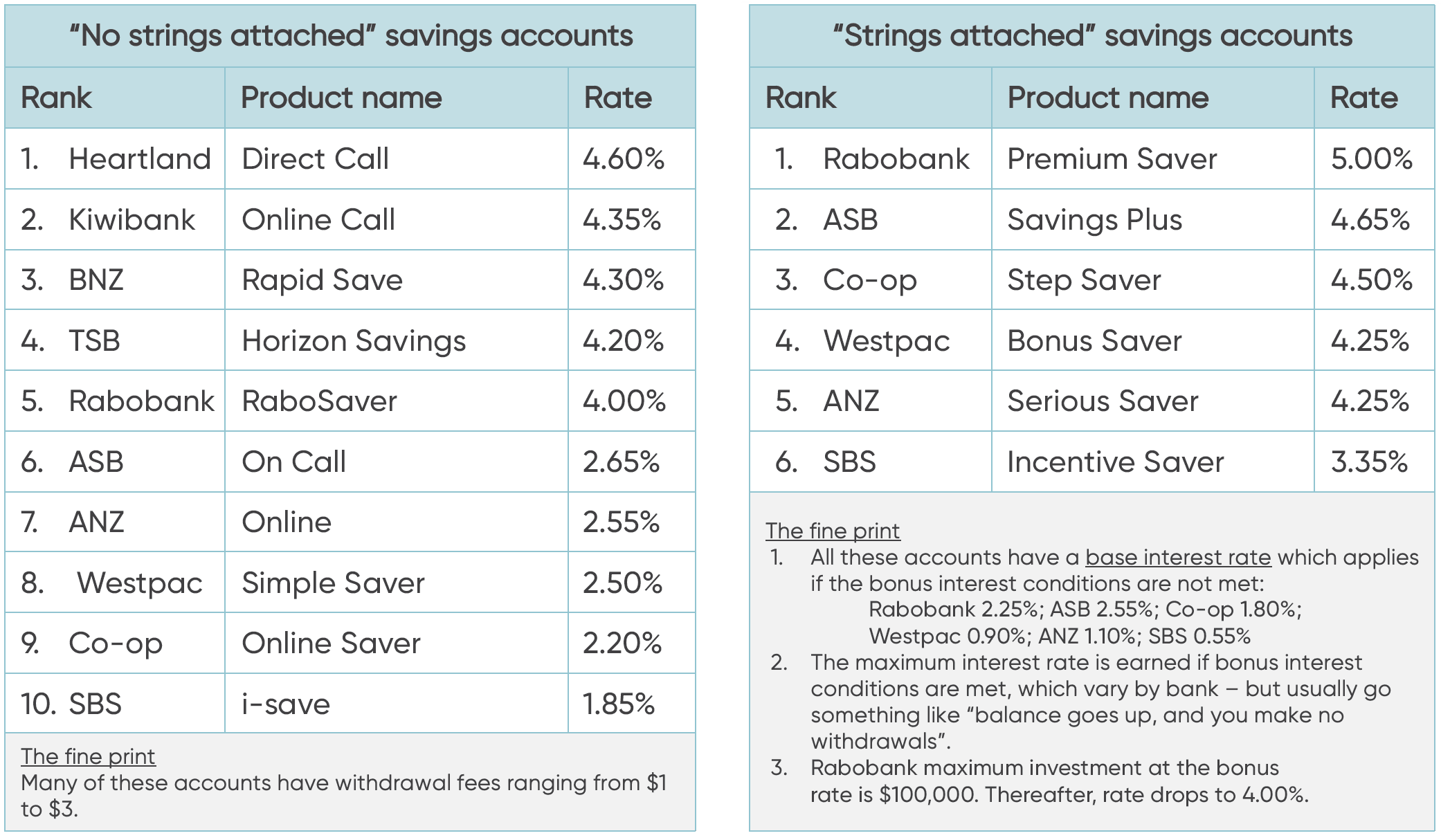

To start with, let’s focus on bank savings accounts, where the money is on-call (so you can withdraw it at any time).

In simple terms, there are two types of bank savings accounts:

- No strings attached.

Where you’ll earn daily interest on your entire balance at one flat interest rate, which doesn’t change based on account activity. Though sometimes you’ll be pinged with transaction fees for withdrawals. - Strings attached.

Where you have to jump through some hoops to earn the maximum interest rate. Abide by the rules (that the bank sets) and the interest is higher. Don’t, and the return is dismal.

We have 10 main retail banks in New Zealand, so I’ve picked the best account from each bank in each of the two categories. Note that some banks don’t have “strings attached” accounts.

Notice Saver and Term Investments

If you’re prepared to lock your money away for a while, you’ll earn a lot more interest. There are two options:

- Notice Saver accounts

Where you’ve got to let the bank know (well) in advance that you want to take your money out – up 32, 60 or 90 days. Kiwibank, Heartland, Rabobank and Westpac all offer Notice Saver accounts, with interest rates that vary from 4.50% to 5.50% depending on the bank. - Term Investments

Terms range from 30 days to 5 years. The interest rates for terms of 30 to 90 days range from 2.25% to 4.4%. Longer term rates are over 5% once you get out to six-month terms and beyond, but of course you’ll need to be prepared to lock your money away for longer.

Squirrel On-Call Account

A recent addition to the savings suite of products is Squirrel’s On-Call account, which pays 5.00% p.a.* with no strings attached.

Every cent of the funds is held on trust in an account with a Standard & Poor’s AA- rated major registered bank. So, it’s similar to a normal bank account, just with better returns.

Funds can be moved between your main bank and Squirrel within two hours on business days, between 9am and 10pm.

You can find out more about the Squirrel On-Call account on our website.

*Accurate as at 19 May 2023.