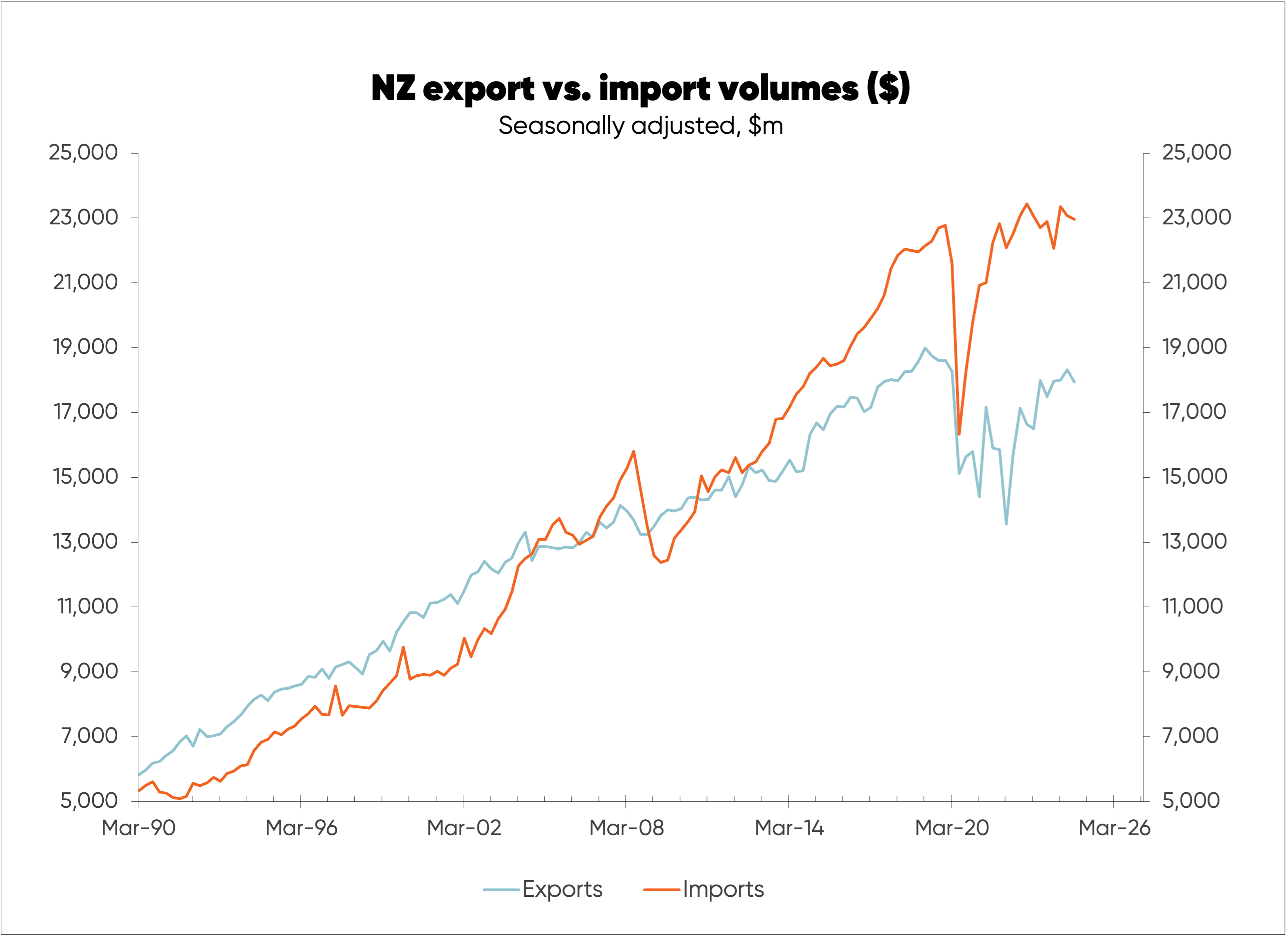

Over the last decade, New Zealand’s export volumes have stagnated, leaving us more reliant on imports. If export volumes had matched growth in import volumes in recent years, Kiwi would be around $5,500 better off per year on average than they are currently.

There are a number of factors behind this stalling in export growth, including the impact of climate policies and a range of traditional agricultural exports faltering. There appears to be no easy solutions (and I have little faith in the ability of governments to pick winners).

Maybe this is as good as it gets for NZ, but hopefully some new export winners emerge over the next decade.

NZ export volumes have performed poorly for most of the last decade and grown much less than import volumes (see the first chart, below). Both goods and services exports have shown limited growth in recent years, and neither have yet rebounded to pre-Covid levels.

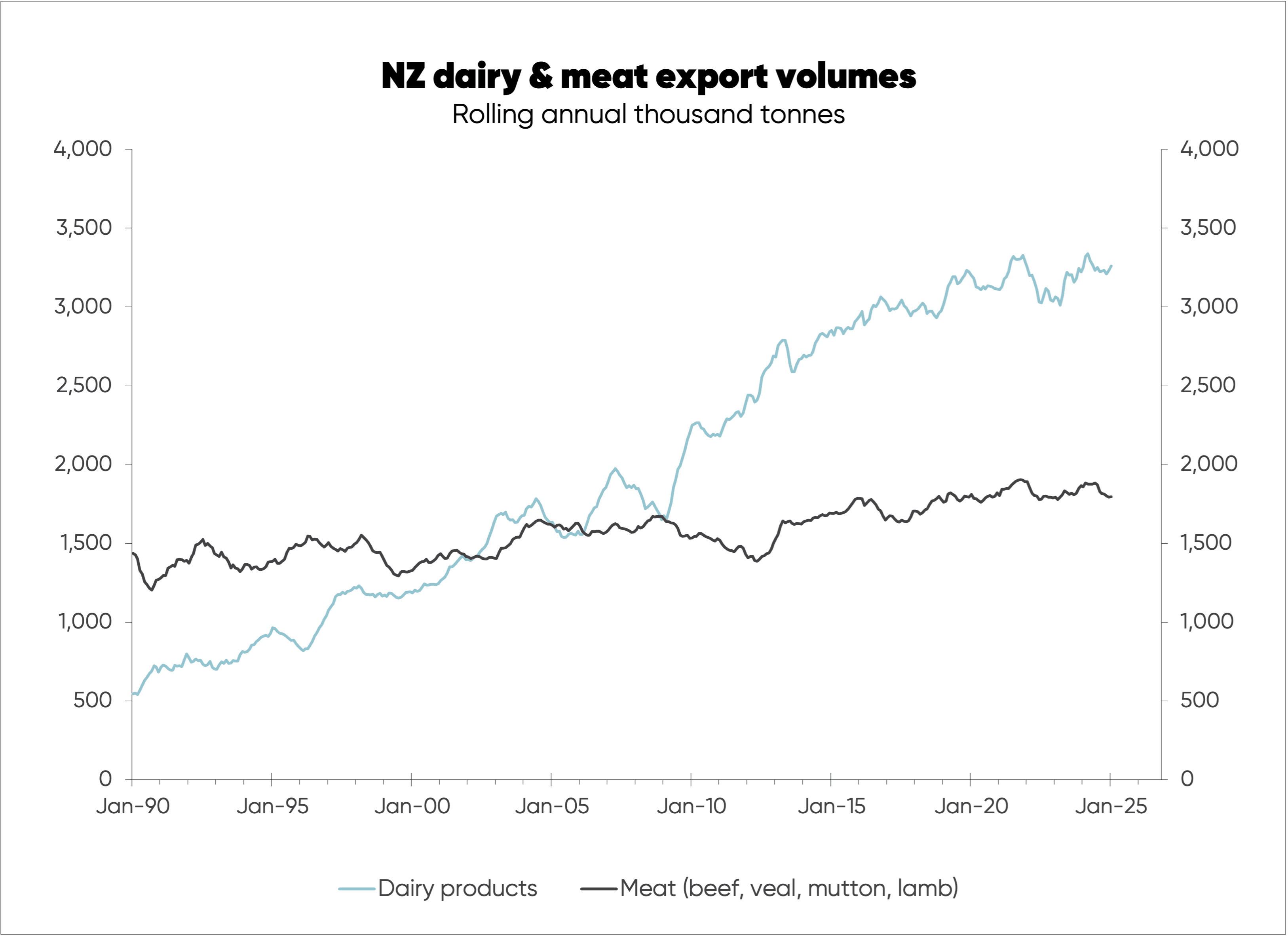

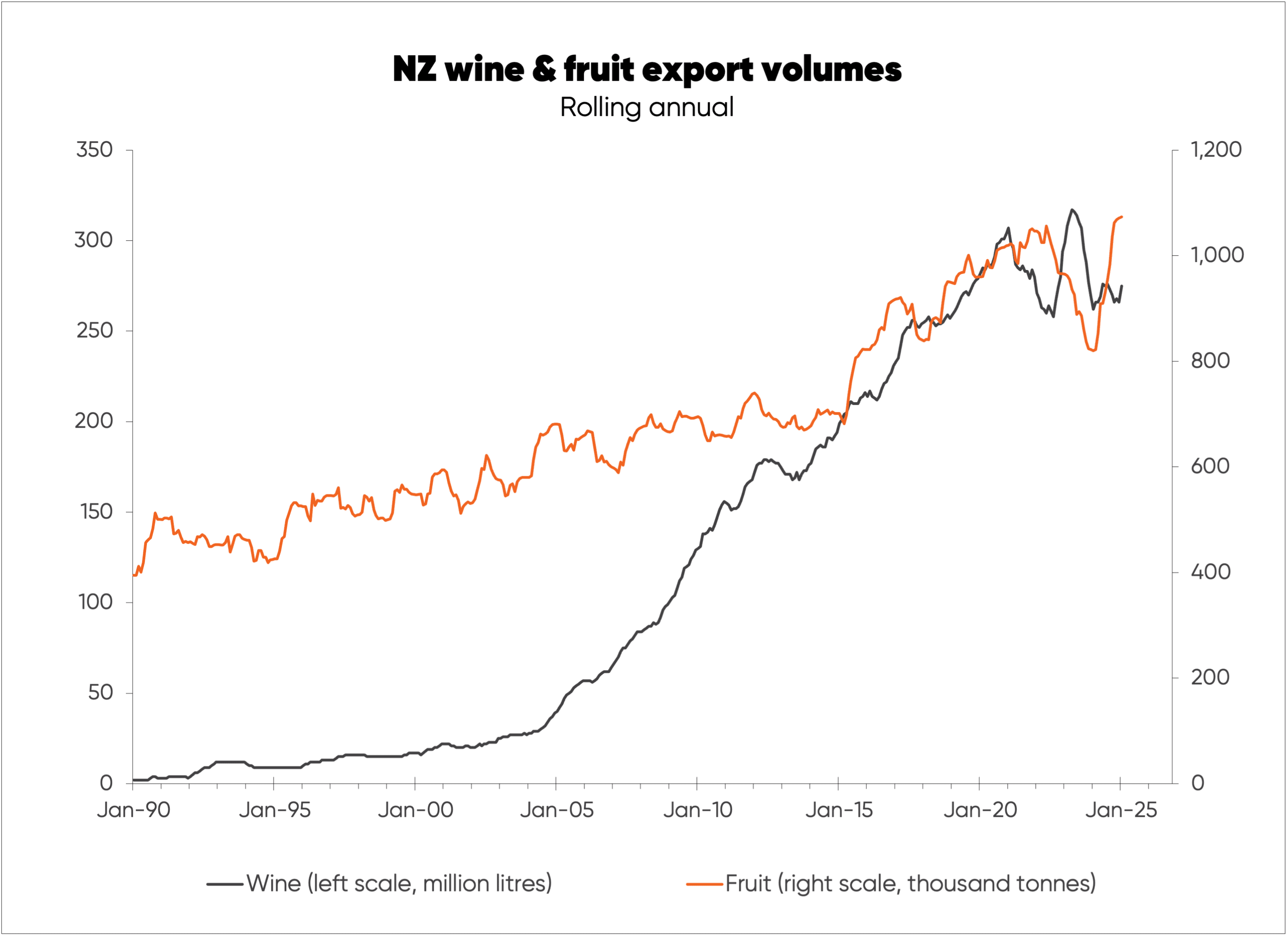

NZ goods exports are dominated by primary products, mainly dairy and meat, but also fruit, wine, and honey. Services exports, meanwhile, are dominated by foreign visitors spending money in NZ—tourist numbers were hit badly by Covid-related border closures, and have not yet recovered to pre-Covid levels.

If export volumes had kept up with import volumes, New Zealand’s total economic activity or Gross Domestic Product (GDP) would be around 6.8% or $29b higher per year in current dollar values. In terms of income, this translates to around $5,500 extra per person per year on average.

Critically, traditional exports have shown little growth in the last decade—as illustrated in the second chart, below.

Growth in meat export volumes stagnated years ago, while growth in dairy export values was doing well largely until climate policies impacted started to have an impact.

After experiencing massive growth from 2005 to 2020, wine export growth has stagnated in recent years. It’s the same story for fruit export volumes, although they at least have rebounded to slightly above pre-Covid levels (see the third chart).

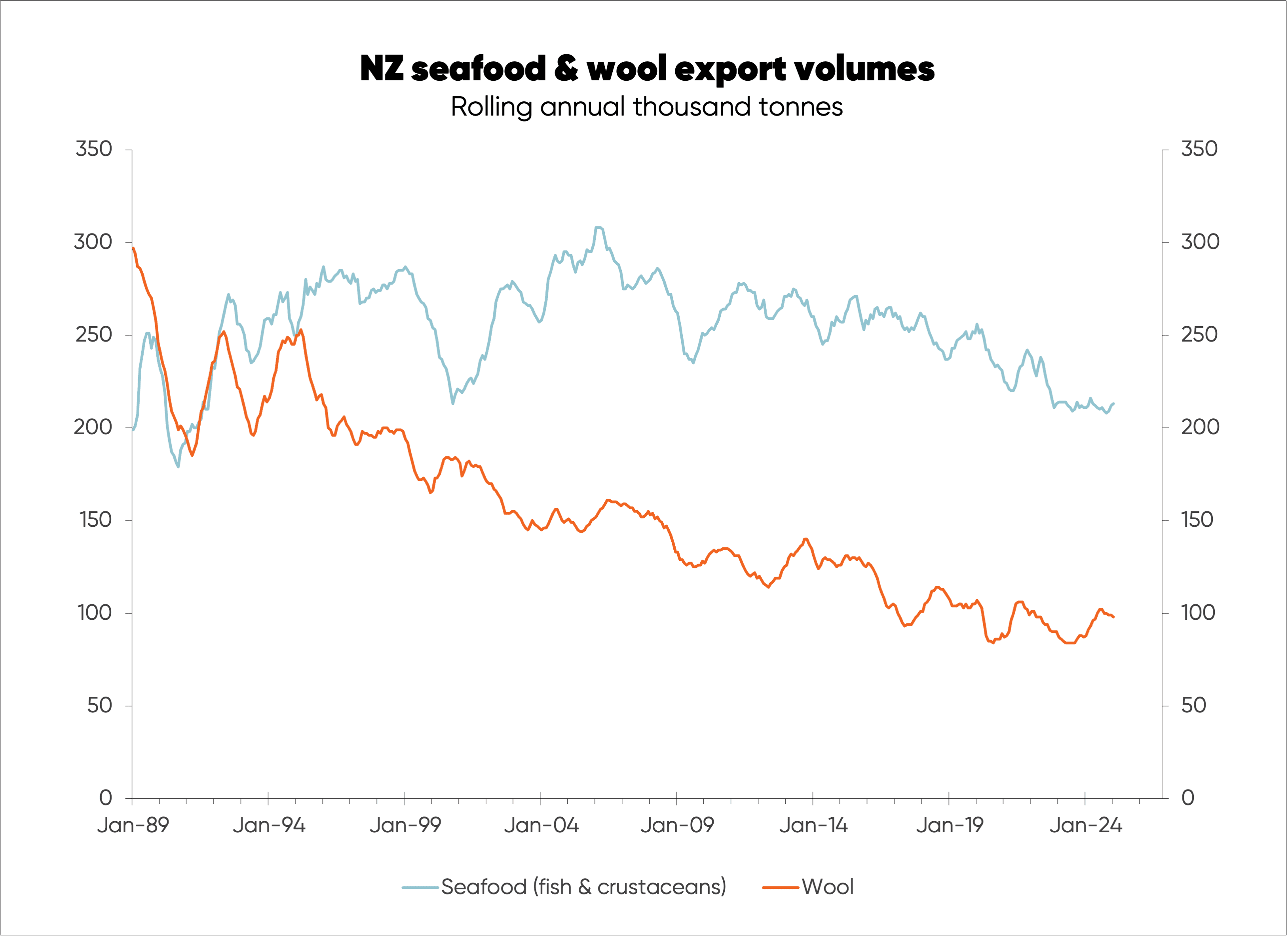

Fish and wool export volumes have been on downward trends for more than a decade (fourth chart).

Forestry export volumes are also still below pre-Covid levels (no chart shown).

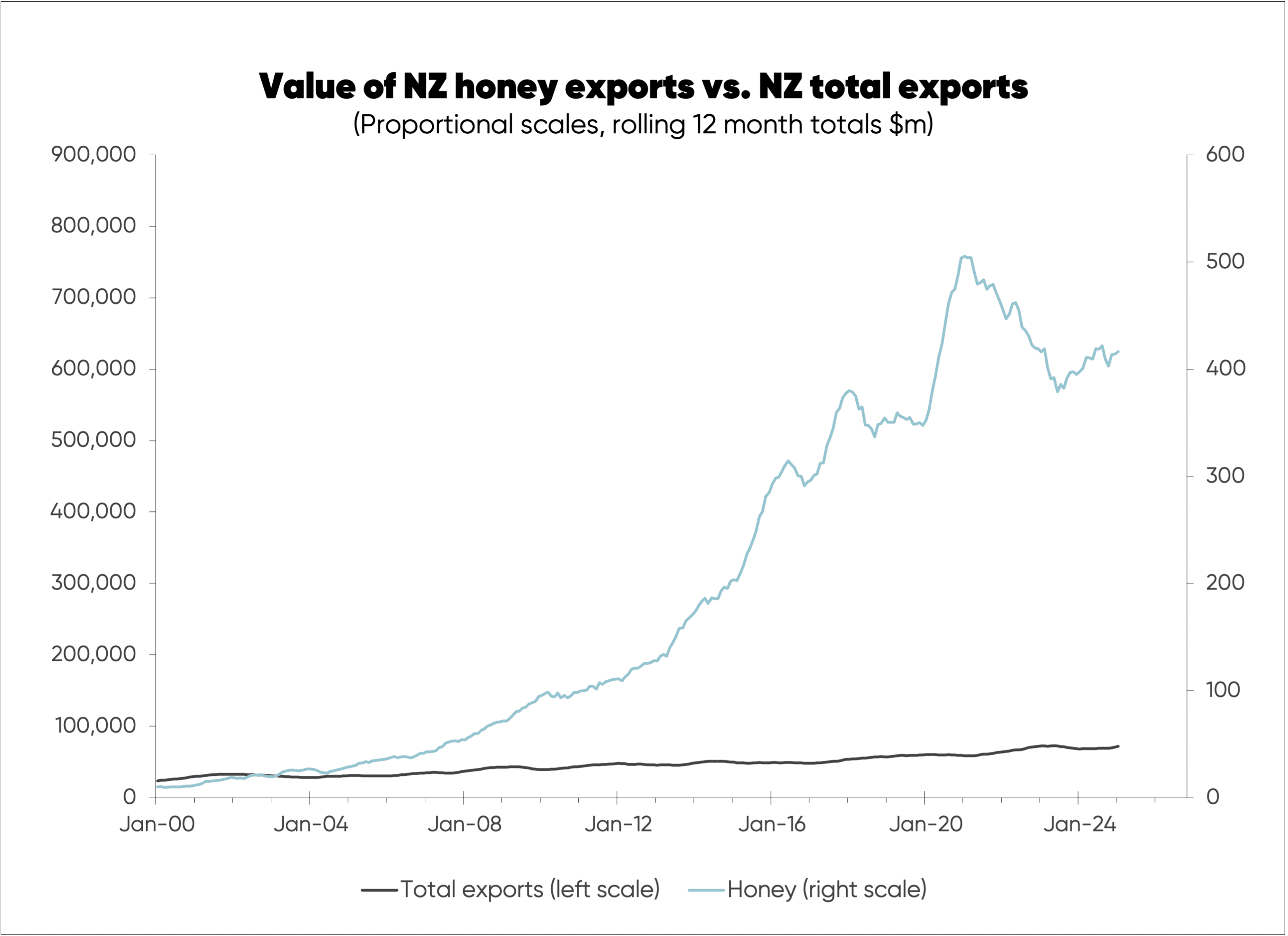

Honey exports were a winner but, again, have suffered since 2020. Export volume data for honey is unavailable, so the fifth and final chart below shows export earnings from honey versus total export receipts for goods (with roughly proportional scales).

“New economy”/IT industries are developing in NZ and a number of these should have strong growth including in exports. But they aren’t big enough yet to change the overall picture. They are included in service exports but may not be measured well.

By Rodney Dickens, Managing Director, Strategic Risk Analysis Ltd www.sra.co.nz.